The use of this site and the content contained therein is governed by the Terms of Use. When you use this site you acknowledge that you have read the Terms of Use and that you accept and will be bound by the terms hereof and such terms as may be modified from time to time.

All text, graphics, audio, design and other works on the site are the copyrighted works of nasscom unless otherwise indicated. All rights reserved.

Content on the site is for personal use only and may be downloaded provided the material is kept intact and there is no violation of the copyrights, trademarks, and other proprietary rights. Any alteration of the material or use of the material contained in the site for any other purpose is a violation of the copyright of nasscom and / or its affiliates or associates or of its third-party information providers. This material cannot be copied, reproduced, republished, uploaded, posted, transmitted or distributed in any way for non-personal use without obtaining the prior permission from nasscom.

The nasscom Members login is for the reference of only registered nasscom Member Companies.

nasscom reserves the right to modify the terms of use of any service without any liability. nasscom reserves the right to take all measures necessary to prevent access to any service or termination of service if the terms of use are not complied with or are contravened or there is any violation of copyright, trademark or other proprietary right.

From time to time nasscom may supplement these terms of use with additional terms pertaining to specific content (additional terms). Such additional terms are hereby incorporated by reference into these Terms of Use.

Disclaimer

The Company information provided on the nasscom web site is as per data collected by companies. nasscom is not liable on the authenticity of such data.

nasscom has exercised due diligence in checking the correctness and authenticity of the information contained in the site, but nasscom or any of its affiliates or associates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this site. The information from or through this site is provided "as is" and all warranties express or implied of any kind, regarding any matter pertaining to any service or channel, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement are disclaimed. nasscom and its affiliates and associates shall not be liable, at any time, for any failure of performance, error, omission, interruption, deletion, defect, delay in operation or transmission, computer virus, communications line failure, theft or destruction or unauthorised access to, alteration of, or use of information contained on the site. No representations, warranties or guarantees whatsoever are made as to the accuracy, adequacy, reliability, completeness, suitability or applicability of the information to a particular situation.

nasscom or its affiliates or associates or its employees do not provide any judgments or warranty in respect of the authenticity or correctness of the content of other services or sites to which links are provided. A link to another service or site is not an endorsement of any products or services on such site or the site.

The content provided is for information purposes alone and does not substitute for specific advice whether investment, legal, taxation or otherwise. nasscom disclaims all liability for damages caused by use of content on the site.

All responsibility and liability for any damages caused by downloading of any data is disclaimed.

nasscom reserves the right to modify, suspend / cancel, or discontinue any or all sections, or service at any time without notice.

For any grievances under the Information Technology Act 2000, please get in touch with Grievance Officer, Mr. Anirban Mandal at data-query@nasscom.in.

The word cross-border refers to payments across different countries. Cross-border payments are vital to individuals, businesses, merchants, industries, and international development organizations. However, cross-border transactions are often inconvenient due to their exorbitant fees and lengthy processing times. The use of blockchain in cross-border payments will make the entire process simpler. The global economy will get an uplift by using blockchain technology for cross-border payments.

Distributed ledger technology or blockchain technology is a game-changer move in cross-border money transfer. It accelerates the payment process by employing encryption technology. At present many blockchain-based payment platforms already exist, and many more will come in the future.

In this blog, we will take a look at the existing cross-border payments system and how blockchain technology is swifter and more efficient. We would also evaluate the major changes that industries foresee and what the future beholds for the use of blockchain in cross-border payments.

How do regular cross-border payments work?

Various global messaging systems operate the traditional international transactions, and it connects a network of banks. A remittance transfer does the transaction. A remittance transfer is a monetary transaction along cross-borders by a company that associates with — banks, credit unions, or financial service institutions.

Majorly, a remittance transfer takes less transaction fee than a bank transfer. In traditional cross-border payments, the ledger isn’t the same between the sender and receiver. Thus, adding a security concern to the whole settlement process. One of the examples of a remittance transfer channel is SWIFT.

It redirects transactions by applying a coded messaging system. Businesses and individuals have to sign-up with a payment service provider to receive an international payment. This acts as a gateway for payment.

While the traditional system often fails on traceability. And due to mediator banks in between, the transaction process becomes cumbersome along with a hefty fee. In addition, the trade differences between countries make the process more complex. There are several legal restrictions in certain countries. The fees or the taxes can be in the form of customs duty or value-added tax, which vary from one country to another.

Why opt for a Blockchain Network for Transactions?

First of all, immutability is not compromised in the blockchain. The centralized authority is replaced here by a decentralized network. Here, a network of nodes verifies the monetary transaction. As in the traditional cross-border payments – due to various detours in bank branches, a simple peer-to-peer transaction becomes more perplexing. Here, the transaction gets completed in real-time in the blockchain network due to fewer negotiators. Various public blockchains are global and can transfer money anywhere in the world.

A lightning node is an L2 scaling solution that executes transactions instantly at a significantly reduced fee on the Bitcoin blockchain. This node runs on top of the full nodes, facilitating payments at affordable fees. Users deploying this node use Raspberry Pi machines instead of computers.

You should know that not all Bitcoin nodes are miners, even though it’s somewhat impossible to separate them.

While it takes on an average 3-5 days for the transaction to occur, there are errors in transactions sometimes, and it fails in between. However, blockchain supports transparency and traceability. The network solves the pain points of a lot of different industries. Simply put, all the transactions are done quickly with a low transaction fee.

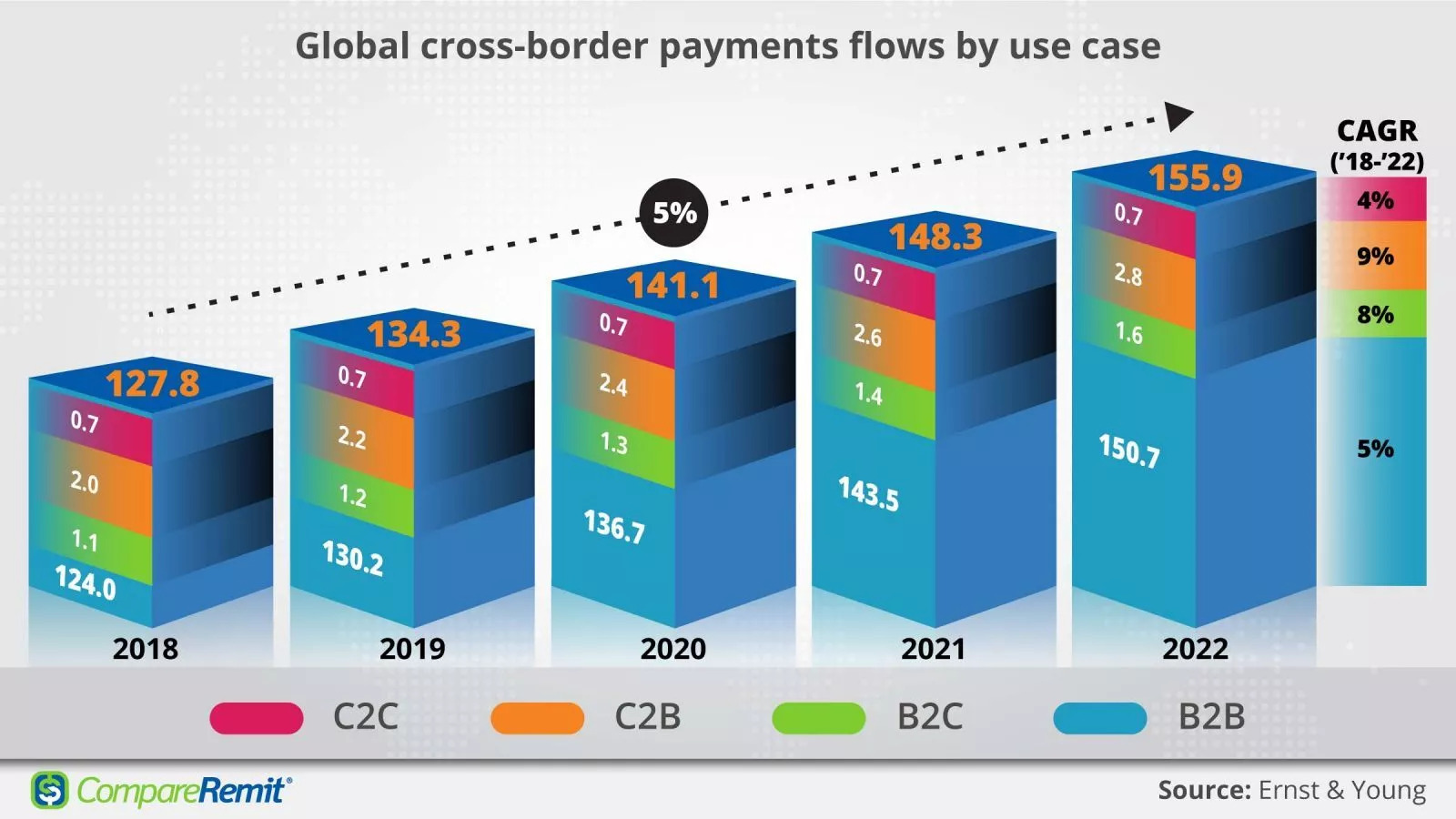

Global Economy of Cross-Border Payments

The global cross-border payments will reach US $156 trillion in 2022. Thus, confirming it as a trillion-dollar market. According to Juniper research, solely the B2B cross-border payments will be a $35 trillion economy in 2022.

Traditionally, the transaction was done by a correspondent banking network (CBN). However, as the technology grows, we witness cross-border payments with distributed ledger technology. According to the world bank report on remittance prices worldwide, the average cost of remittances is around 7%.

In recent years, G20 countries have been on a mission to lower cross-border remittances to 5%. With the emerging trends, organizations such as G20 want more and more countries to participate in the global economy.

As consumers become aware, they are less willing to pay the transaction fee. With the increase in the digital payment methods for remittances, customers are looking for cheap cross-border payment alternatives. And the blockchain has a low transaction fee and can easily accomplish this. The new trendsetters in cross-border payments are countries from North America, Latin America, Asia, and Africa.

Industries thriving on Cross-Border Payments

Multiple examples demonstrate that using blockchain for cross-border payments is faster and more feasible. Banks do the processing of cross-border payments in the majority of the B2B industries. The transactions can be for any individual, banking institution, or industry. The applications can be official development assistance (ODA) for international remittance.

In the past couple of years, B2B industries have been accelerating towards digitization. They are adding so much economy to the global workforce. Only cross-border payments across the USA and UK account for 26% of the total annual sale.

When it comes to understanding industries that can benefit from blockchain in cross-border payments, the list goes on and on.

Still, a few major industries reaping the benefits of blockchain-enabled cross-border payments are – food and beverages, hospitality, accounting, E-commerce, oil and gas, air travel, stock trading, crowdfunding, and many more.

The point to be noted here is that blockchain will not only improve cross-border payments but will also boost the overall health of any industry by securing supply chain management, logistics, etc.

Features of Blockchain

Cross-border payments employing blockchain as its intermediary technology is a significant advantage. Merging the blockchain technology with cross-border payments is a win-win situation for both the sender and the receiver. A few of the features of blockchain technology are:

Non-tampered information

By using blockchain in cross-border payments, tampering with information is difficult. The blockchain architecture has every block with information linking it with the previous block. The database is distributed, and every participant owns a copy of the transactions.

Real-time Payment

For businesses that need funds quickly, real-time payment is a game-changer. The payment happens instantly with transaction information integrated into it. Liquidity management becomes easier in real-time payments for businesses.

Decentralized

In regular cross-border payments, financial institutions follow data privacy regulations. Various banks have different regulations. The flow of clients’ information across various jurisdictions – can be prevented easily by using blockchain technology for cross-border payments.

No intermediaries

Blockchain establishes direct contact between the sender and the receiver. The receiver has direct access to the payment. There are no delays, unnecessary fees, or remittances involved.

There is efficiency with many advantages, and the security is beefed up. The blockchain network solves the credit barriers exceptionally. Overall, it provides a framework for cross-border transactions.

How blockchain works for payments

Here, the two crucial parts of the transaction are the gateway and the customer; no banking institution in between. A person living in the US can send money to Italy using an on-ramp service provider.

The provider will convert the Fiat money into cryptocurrency. The cryptocurrency can be kept in a crypto wallet. One can find multiple crypto wallets, choose anyone, and set up an account; after that, one can initiate the transfer from a bank or credit card.

Finally, you need to have the address of the receiver’s wallet to send the required amount to the receiver. Once the money reaches the receiver’s wallet, the receiver can convert it into fiat money after receiving the cryptocurrency. Crucial steps to transfer money are:

A consumer or a business wants to purchase a product or a service. Here we require consumer ID, retailer ID, amount of transaction, and timestamp.

Smart Contracts are for implementing currency exchange according to the real-time exchange rate.

On the block recording of all the information regarding the transaction is done.

The information in the block is added to the blockchain consensus mechanism by following a technical regulation.

The value of the previous block’s hash is added to the new block. This is an essential step to making the chain tamper-resistant.

The same information is updated on the node as well. The node broadcasts the information further. The block gets verified.

Finally, the transaction is completed, and the cryptocurrency reaches its destination.

Significant changes due to Blockchain-enabled Cross-Border Payments

Even the major mainstream financial companies have started to use the blockchain to pilot transactions. The upper layer technology remains the same, and a little tweak in the core makes it work on blockchain.

In the future, the whole scenario will divide into two types where either the mainstream financial institutions will use blockchain networks in a centralized form. Or blockchain companies completely changing the existing currencies with cryptocurrency.

If the latter happens, stablecoins will also play a role in the transaction process. More and more stablecoins will become popular. As volatility is always in crypto, many users are hesitant to use it. Thus, stablecoins will be helpful to balance the volatility.

Also, government organizations are steadily deploying blockchain technology to manage financial settlements, enhance existing legal frameworks, and grant disbursements.

Advantages of Blockchain Operated Cross-Border Payments

Cross-border payments employing blockchain as its intermediary technology is a significant advantage. With the onset of online business, there has been a surge in cross-border payments. A few of the advantages related to using blockchain in cross-border payments are:

Faster settlement

Any blockchain-enabled cross-border payment takes a few seconds or minutes. Unlike regular payments, which take 3-5 business days. Various issues such as time-zone differences and currency value differences do not affect the transaction time as the cryptocurrency is a globalized currency. The average time is somewhere in the range of 141 minutes to six minutes. When all the transactions happen online, it eliminates the burdensome office activities.

Cost-Effective

Banks have to take the help of intermediary banks to process the transaction. As often, banks don’t have an alliance with the bank in the other nation.

The third party in between charges a fee, and the cost is divided between the sender and the beneficiary. When using a blockchain network for cross-border payments, the transaction fee will only be there for the blockchain network operator.

Enhanced Security

As in the cryptocurrency network, everyone owns a private key. The key acts as a digital signature, and if there is any reason, the system gets hacked. The signature will itself become invalid. As we know, the blockchain is synced simultaneously. Thus, an attacker would not be able to access the information across multiple computers quickly.

Improved Transparency

In the future, traditional financial reporting companies will become obsolete. As in blockchain technology, every transaction and holdings are easy to view on an explorer. Even for a private permissionless blockchain, the participants involved can view the transactions. The entries in the system are validated. By sharing the information across the platforms, there will be a reduction in data discrepancy.

Challenges and Closing Thoughts on Blockchain for Cross-Border Payments

The major challenge is that the majority of the citizens are still not well-equipped with the technology. There isn’t much clarity regarding the regulation of the cryptomarket. The Fintech giants such as Wise or SWIFT are currently hesitant to use distributed ledger technology. These payment platforms will deploy blockchain networks when more and more central banks adopt the distributed ledger technology for cross-border payments.

Honestly, banks are not ready to accept the volatility of crypto. It is one of the major reasons for financial institutions not deploying the blockchain for negotiations. Therefore SWIFT has started the new GPI system for settling the transaction. Recently, SWIFT has also collaborated with RIPPLE to streamline the payments from the blockchain.

Blockchain in cross-border payments is increasing day by day due to many shortcomings in the traditional methods. Blockchain technology will leave a profound impact on cross-border payments structure. It can be a technological breakthrough as there is a gradual weakening of the existing payment models. Although, research and experimentation are a part of emerging trends. We are sure that this will leave an overall positive impact on cross-border payments.

About The Author

Dr. Ravi Chamria is co-founder CEO of Zeeve Inc, an Enterprise Blockchain company. He has an experience of 18+ years in IT consulting spanning across Fintech, InsureTech, Supply Chain and eCommerce. He is an executive MBA from IIM, Lucknow and a prolific speaker on emerging technologies like Blockchain, IoT and AI/ML.

Passionate About: Blockchain, Supply Chain Management, Digital Lending, Digital Payments, AI/ML, IoT

That the contents of third-party articles/blogs published here on the website, and the interpretation of all information in the article/blogs such as data, maps, numbers, opinions etc. displayed in the article/blogs and views or the opinions expressed within the content are solely of the author's; and do not reflect the opinions and beliefs of NASSCOM or its affiliates in any manner. NASSCOM does not take any liability w.r.t. content in any manner and will not be liable in any manner whatsoever for any kind of liability arising out of any act, error or omission. The contents of third-party article/blogs published, are provided solely as convenience; and the presence of these articles/blogs should not, under any circumstances, be considered as an endorsement of the contents by NASSCOM in any manner; and if you chose to access these articles/blogs , you do so at your own risk.

Zeeve is an enterprise-grade Blockchain Infrastructure Automation Platform. Join the growing list of clients that trust us with their Blockchain initiatives

The future of metaverse development for connecting virtual worlds is poised to be an exciting and transformative journey.

Here are some key aspects that may shape its future:

1. Interoperability: One of the major goals of metaverse development…

Personal chats, pictures and videos data are stored on centralized servers. As a result, central servers could see what has been contained in the message. But end-to-end encryption safeguards against such odds by giving complete privacy while using…

Blockchain technology has undoubtedly revolutionized various industries, promising enhanced security, transparency, and decentralization. In the rapidly evolving landscape of blockchain technology, one of the most pressing challenges faced by…

The concept of metaverse development has been gaining significant attention in recent years. It represents a virtual world where users can interact with a computer-based environment and other users in real time. With the rise of blockchain…

The rapid emergence of blockchain has favored many industries. The disrupting technology allows you to build in public and makes your work trustless and secure. It makes the connection between companies and their users better.

Among many of the…

NFT technology is currently transforming digital ownership across various industries, including the art world, gaming, fashion, major businesses, and high-profile celebrity merchandise. However, the impact of NFTs goes far beyond owning digital…