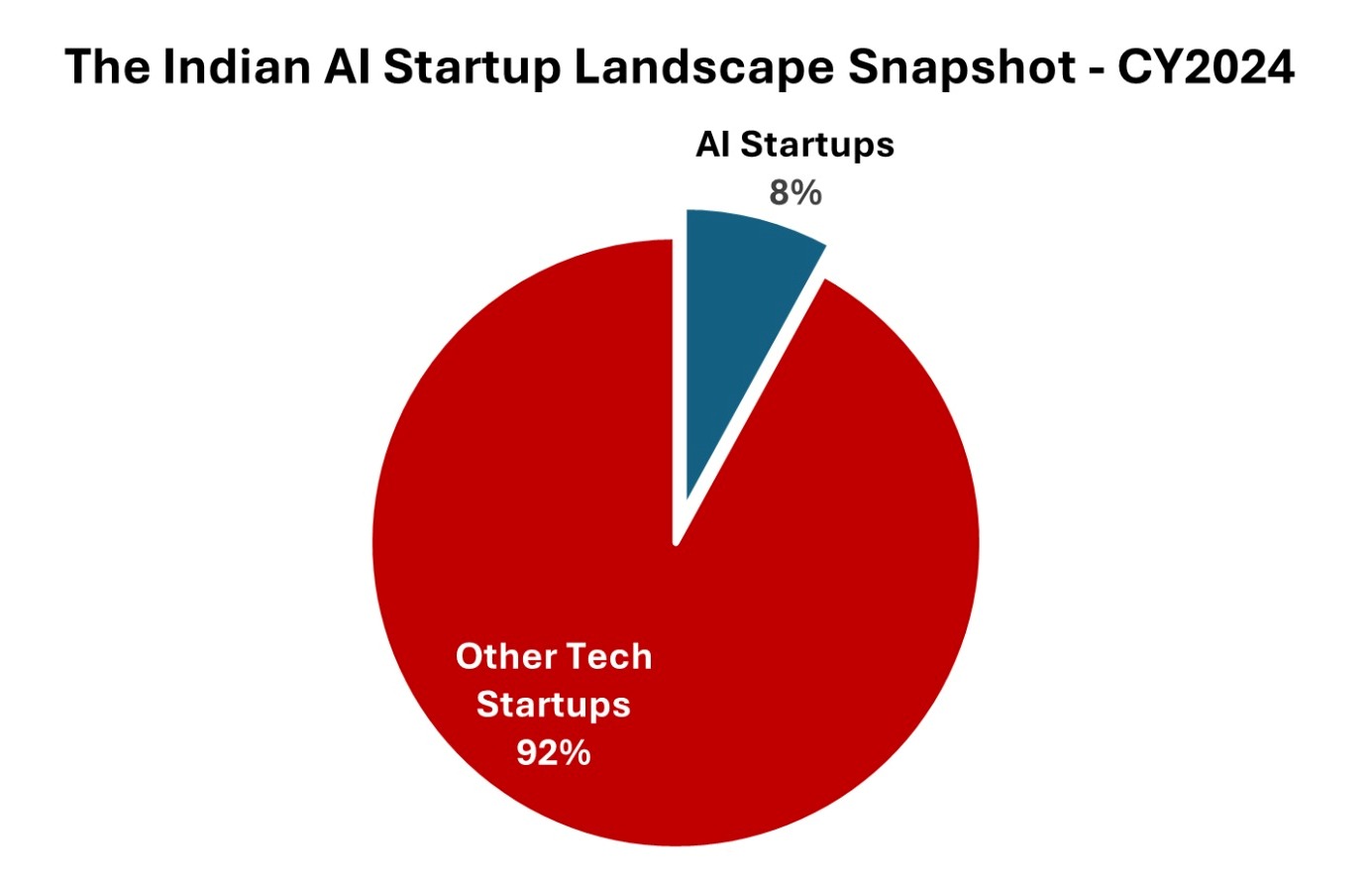

Over the past decade, India’s overall tech startup ecosystem has expanded from around 2000 tech startups in 2014 to 32,000-35,000 active startups in 2024, underpinned by more than $60 Bn in cumulative funding only in the last five years and 80+ active unicorns in the space. Within this universe, DeepTech startups have grown faster than the rest – now numbering ~4,000 and clocking 78% y-o-y funding growth in 2024. AI startups, a subset of DeepTech, have risen sharply across multiple hubs. While Bangalore continues to wear the crown of India’s AI capital, a closer, more strategic look at the data reveals a more dynamic and evolving picture. For long, we have seen how early momentum, when matched with the right enablers, can shift the axis of innovation. Today, there are clear signals that the gravitational pull of AI entrepreneurship in India may slowly be tilting, opening a window of opportunity for India’s policymakers, investors, industry bodies, and innovation enablers to make proactive, future-aligned choices.

By splitting the 2015–24 period into three phases, we see distinct momentum shifts:

|

Period

|

Avg. Annual AI Startup Growth

(across Bangalore, Delhi-NCR, Mumbai, Hyderabad, Pune, and Chennai)

|

Key Drivers

|

|

2015–20

|

15%

|

- The launch of programs like Digital India and Startup India provided a supportive environment. For instance, the Atal Innovation Mission (AIM) established numerous Atal Tinkering Labs across the country, fostering innovation and entrepreneurship.

- Institutions like the IITs and IIITs ramped up AI research. For example, IIT Madras launched the Robert Bosch Centre for Data Science and AI (RBCDSAI) in 2017, which became a hub for AI research.

- Companies like TCS and Infosys began integrating AI into their operations, creating a demand for AI solutions and encouraging startups to fill these gaps.

- Growth in funding support from VCs. For example, Niki.ai, an AI-based chatbot startup, raised significant funding from investors like Ratan Tata and Unilazer Ventures

|

|

2021–22

|

-28%

|

- The COVID-19 pandemic accelerated the adoption of digital technologies. Startups like Caare, which developed AI solutions for bridging healthcare gaps in marginalized communities, saw increased demand for their products during the pandemic.

- Indian AI startups started gaining international traction.

- Continued support from government policies, such as the National AI Strategy, aimed at positioning India as a global AI hub.

- Rapid advancements in AI technologies enabled startups to identify more whitespaces and develop more sophisticated solutions.

|

|

2023–24

|

81%

|

- The rise of generative AI technologies led to a surge in startups focusing on this area.

- Innovation hubs emerged in smaller cities. For example, around 40% of the new tech startup creation in CY 2023 happened in emerging hubs, with AI accounting for a significantly large share.

- Indian AI startups continued to expand globally. Fractal Analytics, for instance, established itself as a key player in the international market and formed strategic partnerships with global tech giants.

|

Here's a more detailed snapshot of where India stands today in terms of AI startup hubs:

- Bangalore: 700+ AI startups | 10% CAGR (2015–2024) | 20% avg. y-o-y growth

- Delhi-NCR: 500+ AI startups | 8% CAGR (2015–2024) | 26% avg. y-o-y growth

- Mumbai: 250+ AI startups | 3% CAGR (2015–2024) | 10% avg. y-o-y growth

- Hyderabad: 150+ AI startups | 4% CAGR (2015–2024) | 10% avg. y-o-y growth

- Pune: 100+ AI startups | 5% CAGR (2015–2024) | 26% avg. y-o-y growth

- Chennai: 80+ AI startups | 7% CAGR (2015–2024) | 29% avg. y-o-y growth

- Emerging Hubs (e.g., Ahmedabad, Jaipur, Coimbatore, Lucknow): 10–60 AI startups

These are not just numbers – these are signals of emerging market behaviour, founder mindsets, policy impact, and investment direction. If listened to closely, these numbers tell a compelling story.

5 Strategic Insights Not Clearly VisibleonThe Surface

1. Bangalore Still Dominates, But Its Growth Is Maturing

Bangalore AI Startup Ecosystem Dynamics: From 2015-18, Bangalore saw double‐digit y-o-y growth, fuelled by early VC enthusiasm and government schemes. The 2021–22 slump (-45%, -20%) reflects a temporary pivot toward pandemic‐response startups and capital flight from high‐burn AI R&D. The 173% rebound in 2023, driven by generative AI, followed by a more modest 16% in 2024 shows the ecosystem shifting from raw formation to a focus on scaling, exits, and consolidation.

What this means:Bangalore's dominance is undeniable.With 700+ AI startups, Bangalore leads India’s AI landscape by a comfortable margin – over 40% more than its nearest peer, Delhi NCR (500+). Its 10% CAGR (2015–24) shows steady, sustainable growth, while an average 20% y-o-y uptick shows it remains a fertile ground for new AI startups, supporting its reputation as the country’s “AI factory”. On zooming out a bit, thisgrowth easing to 10% CAGR (2015–24) and 20% avg. y-o-y reflects ecosystem maturity and focus on late-stage scaling.This hints towards Bangalore becoming a consolidation hub, where startups scale, raise late-stage capital, and exit. But it is no longer the only magnet for early-stage AI innovation.

2. Delhi-NCR Is India’s Most Underrated AI Frontier

Delhi-NCR AI Startup Ecosystem Dynamics: Initial AI growth was uneven (-27% in 2016, +21% in 2017), stabilizing in 2018-20 (+8%, +33%, +25%). The pandemic-induced drop (-38% in 2021, -50% in 2022) echoes Bangalore’s pattern but was followed by a 232% spike in 2023 and 27% in 2024, indicating investor recognition of Delhi-NCR’s strengths.

What this means:The data around Delhi-NCR is particularly striking.500+ AI startups, an 8% CAGR between 2015 and 2024, and a massive 26% average y-o-y growth highlight this region as a rapidly maturing AI hub. This delta between long-term and short-term momentum (as indicated by CAGR and average y-o-y growth rate respectively) tells us something profound – Delhi-NCR’s AI ecosystem has exploded in the past 2–3 years, and if nurtured properly, it could rival Bangalore’s scale over the next 3–5 years.

This is not accidental. Rather,it reflects the strength of the region’s academic institutions such as IIT Delhi, IIIT Delhi, etc. This also means that investor interest in Delhi-NCR is no longer playing catch-up – rather, it is shaping its own unique AI narrative, with focus spanning across sectors such as governance, health, education, and industrial automation among others.

3. Chennai and Pune Emerge As Hidden AI Growth Engines

Chennai AI Startup Ecosystem Dynamics:After stagnant early years (0% in 2016, -33% in 2017), Chennai’s AI startup ecosystem exploded in 2018 (+267%) and weathered oscillations before a 57% surge in 2023 and 55% in 2024. This “late-cycle boom” arises from a confluence of multiple forces, such as automotive AI labs, edge-computing startups, Tamil Nadu’s targeted tech parks, etc.

Pune AI Startup Ecosystem Dynamics:Pune’s y-o-y swings (+69% in 2017, +73% in 2019, +120% in 2023, +91% in 2024) reflect episodic VC interest. Despite a smaller count, the 26% average y-o-y indicates a robust mid-sized hub that blends enterprise heritage with deep-tech agility.

What this means:While often overlooked, both Chennai (29% y-o-y) and Pune (26%) are seeing breakneck growth in the number of AI startups, especially off a small base.

Chennai’s stronghold in industrial AI, automotive, and edge computing (with players in AI hardware and robotics) is getting stronger. Pune, with its mix of enterprise IT heritage and newer SaaS + AI startups, is attracting early-stage capital and AI technical talent. Hence, these cities represent India’s second AI wave.What Bangalore was 15 years back, these hubs are today, and strategic investments here could deliver asymmetric returns.

4. Mumbai and Hyderabad Show Signs of Plateauing Growth

Mumbai AI Startup Ecosystem Dynamics:Mumbai’s early leads (+42% in 2016) faded to a plateau (+0% in 2017, -21% in 2018), with a 100% rebound in 2023 but only 25% in 2024. Startups like Haptikare based out of this location, but the city’s AI growth seems tethered more to fintech and adtech demand than core DeepTech R&D.

Hyderabad AI Startup Ecosystem Dynamics:Despite +38% in 2017 and +75% in 2023, a -55% drop in 2021 and modest +5% in 2024 signal that state incentives (T-Hub, Genome Valley, etc.) have yet to generate sustained founder momentum or talent retention, suggesting the need for deeper ecosystem orchestration.

What this means:Mumbai’s 3% CAGR and Hyderabad’s 4% CAGR, both paired with just 10% y‑o‑y growth, suggest these markets are approaching maturity or facing saturation. While Mumbai’s AI ecosystem is more finance- and marketing-led than DeepTech-driven, Hyderabad, despite strong state support, needs more sustained founder momentum and ecosystem orchestration to retain early AI talent.Founders and investors might need to look beyond these established hubs for untapped AI opportunities or strengthen the existing local ecosystems through new policy incentives, deeper corporate‑startup partnerships, and other strategic moves.

5. A Shift Toward Emerging Cities

Cities like Ahmedabad, Jaipur, Kolkata, Coimbatore, and Kochi, while still hosting smaller AI communities, have all crossed a crucial threshold – from zero to viable AI ecosystems.

These are not isolated players anymore, andif strategically nudged, they could power regional innovation, serve localized use cases (agriculture, healthcare, logistics etc.), and bring India closer to its inclusive AI vision.

The Case for a Distributed AI Innovation Network

Clearly, Bangalore remains essential as a scale and exit hub – with unmatched deep engineering talent and capital density. Emerging hubs like Delhi-NCR (26% avg. y-o-y growth), Pune (26% avg. y-o-y growth), and Chennai (29% avg. y-o-y growth) are where raw momentum is the highest and greenfield opportunities abound. Hence, strategic diversification – not abandonment of Bangalore – is the way forward. In fact, rather than trying to duplicate Bangalore’s entire ecosystem, India can cultivate specialized nodes by analysing the location-specific academia focus, investor focus, government focus, innovation infrastructure strength, etc. and creating strategy, to boost the growth of tech startup ecosystem within that region, accordingly. By guiding capital and policy to high-growth nodes, India can build a resilient, pan-Indian AI powerhouse.

Action Agenda for Stakeholders

- Policymakers:

- Customize incentives for Delhi-NCR, Chennai, Pune, and selected Tier-2 hubs.

- Expand regulatory sandboxes and talent programs in these fast-growing regions.

- Investors:

- Allocate dedicatedDeepTech/AI funds to high-potential emerging hubs.

- Partner with local incubators to spot early-stage opportunities.

- Industry & Academia:

- Establish hub-specific CoEs in public institutions (IITs, IIITs) outside Bangalore.

- Encourage corporate R&D labs to set up satellite centers in high-momentum cities.

- Industry Associations:

- Foster cross-hub collaboration via national forums, hackathons, and exchange programs.

- Showcase success stories from diverse hubs to shift perception and attract talent.

Future Outlook& Strategic Imperatives

- We expect Bangalore toretain its critical role as the scale & exit node, essential for late-stage funding, high-value DeepTech, and global corporate R&D partnerships.

- Delhi-NCR, Chennai, and Pune can be where raw growth momentum and sectoral specialization converge, making them prime locations for next-gen AI breakthroughs.

- Startups solving strategic technology gaps (semiconductor design, space tech, climate change, etc.) and building scalable businesses around them will attract more government-backed growth capital and international partnerships.

- If required interventions, to support the AI startup ecosystem in hubs beyond Bangalore, are executed in a timely manner, domestic capital will increasingly favour emerging hubs with high y-o-y growth.

Analyst’s Final Thoughts

Bangalore remains indispensable as the scale and exit centre, but the raw momentum of Delhi-NCR, Chennai, and Pune, each sustaining 27–30% avg. y-o-y growth, demonstrates that India’s AI story will be written across multiple specialized hubs.Bangalore’s slowdown, in terms ofnew AI startup creation, is not a sign of decline, but of maturity. Over the years, Bangalore has evolved from being the nursery of startups to the accelerator of scaled AI enterprises, which is a natural, healthy transition in a truly mature innovation ecosystem.On the other hand, Delhi-NCR, Pune, and Chennai are no longer "emerging hubs" in a simplistic sense. They are active epicenters of early-stage AI innovation, each driven by distinct structural enablers. Their rising share in net new startup creation hints towards a future where India's next AI breakthroughs will emerge from a distributed geography, not a single mega hub.

If policymakers, investors, and academia continue to think in terms of "strengthening Bangalore," they risk misreading the moment. The imperative now is not just to build ‘one bigger Bangalore’, but to architect a multi-nodal innovation network, where each city deepens its specialization and connects synergistically with others, maximizing collective strength. In the long term, India’s ability to lead globally in AI will be determined less by the absolute size of any one city’s ecosystem, and more by the resilience, adaptability, and complementarity of its distributed hubs. By aligning policy incentives, capital deployment, and corporate R&D across this distributed network, we can forge an ecosystem that is resilient to shocks, inclusive, and positioned for global leadership. The question now should be, “What should be the differentiated AI policy and infrastructure blueprint for each of these rising hubs, based on their unique sectoral strengths, instead of one-size-fits-all national AI policies?”

Comment

The report challenges traditional notions of AI development hubs, suggesting that emerging cities may become new centers of innovation. Factors like cost-effectiveness, talent availability, and supportive ecosystems contribute to this shift. As AI continues to evolve, what strategies can lesser-known regions adopt to position themselves as attractive destinations for AI investment and development.