A three-decade-long transformational journey of Indian retail

When I started my career in the mid-’90s in an old British multinational company, I was told about the golden days of the past. A sales officer would have a Permanent Journey Plan, referred to as a PJP, across 25 towns in a month to connect to the local distributors. A postcard would be sent to all distributors with details of their PJPs and they would then book a train passing through all these stations to meet and greet their stakeholders. When the train would halt at the station mentioned in the journey plan, the local distributor would be standing with refreshments and an order sheet. He would take extra care of the officer so that all his ordered goods would be supplied. The Sales Officer without stepping out of the platform would complete his transaction and move on to the next town.

Those were the days of shortages and supply led distribution.

Change is the only constant, and we saw it coming

As the ’90s came everything about the distribution strategy of companies in India started to change. Bursting with the promise of a huge untapped Indian market, some of the largest consumer goods companies jumped in, with the FMCG sector witnessing following five key developments:

- Grand entry of giants synonymous with Colas – Coke, and Pepsi, opening the market to Globalization and starting the eminent cola war

- Other global consumer goods companies like P&G, Henkel, Perfetti, Wrigley’s, and Nivea entered the newly attractive Indian marketplace. This kickstarted an evolution determined to change the face of how consumer goods were distributed, sold and bought in the country

- These new entrants posed competition for Indian companies like ITC, Godrej, and Dabur among others and entrenched MNCs like Cadbury’s and Nestle; necessitating them to reinvent their distribution strategy to stay in the game

- The next phase was the beginning of market consolidations to realize distribution, procurement, and marketing synergies. P&G and Godrej formed a joint venture called P&G Godrej to leverage Godrej’s scale & distribution, though the experiment came to a quick end three years later. In another instance, Tata Oil Mills Company Ltd. (TOMCO) was acquired by Hindustan Lever Ltd. (HLL) with the objective of market expansion. One of the biggest consolidations in the sector took place when Hindustan Lever merged Ponds India and Brooke Bonds to form a singular Unilever entity, represented by HLL

- In 2005 came Dabur India’s acquisition of Balsara Hygiene and Home Care businesses to capitalize on the consolidation in the sector. Mergers and acquisitions stabilized the sector distributing considerable market share among big players; though these came with unique approaches in all cases. Coca Cola, for example, had an initial strategy to buy out Parle, a large home-grown player with the famous Thums up, Goldspot, Limca, and Citra in its kitty, and replace these brands with brands from the Coca Cola stable. However, over a period of time and after many failed attempts, Coca Cola realized that Thums Up’s brand equity was too strong to be demolished. Coca Cola pivoted its plan and started investing in the brand, and today Thums Up remains the most powerful brand in the Coca Cola house in India

- Lastly, modern retail chains began to emerge as the market matured, starting from the south of the country and then moving upwards. These replaced the traditional Kirana stores that earlier ruled the roost but were a huge limitation for brands and consumers alike. Largely thanks to the cola wars, even normal grocery outlets got exposed to concepts like extra discounts and paid-up visibility, while newer retail concepts gave it steam.

“The ’90s and early 2000s were focused on growth driven through the expansion of distribution. It was the calm before the digital rush.”

The age of custom distribution strategy in India

From the days of supply-oriented distribution in a country facing scarcity of options, run under the notion of supply creating its own demand, we have traversed a long way to reach where we stand today. This is all attributed to the work done by many consumer brands and FMCG players over the years, for today’s consumers to be spoilt for choice in a highly competitive market.

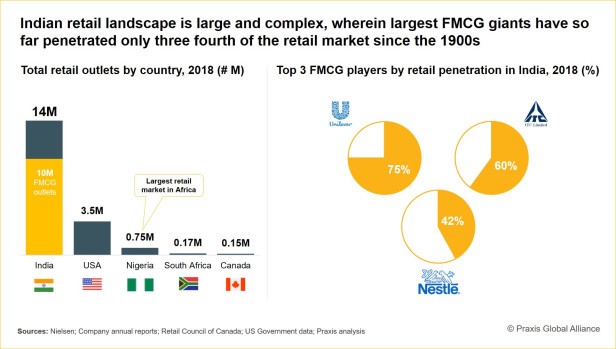

Today if a new brand is to be launched or a multi-brand company has to launch a new variant, the distribution strategy has to be carefully crafted based on the target consumer. This has its own impact on distribution, which is becoming highly curated and increasingly hyperlocal. If you are launching a mass product like ‘Glucose Biscuits’ for example, your objective is to reach the maximum number and forms of outlets including grocery or Kirana shops or local convenience stores, confectionery outlets, roadside tea or cigarette stalls which are quick snack bars for daily commuters, or even nudge the product to be added to a basket of goods the customer may buy online. While wholesale penetration is highly important, the discovery of points of decision making and consumption becomes crucial here. This is why, in an ever-changing Indian retail landscape, even the topmost FMCG companies including HUL, Nestle, and ITC still have some way to go before they realize full retail penetration, highlighting the complexity of the Indian retail market.

However, if you are launching a top-end fitness product, then your distribution strategy would only include key outlets in select areas of the top 25 towns based on the price of the product. This niche distribution would also be highly focused on experience given the disparate and increasing Purchasing Power Parity of Indian consumers.

A lot has changed in the top consumer segment

For the FMCG segment particularly, supermarkets including Modern Bazar, Big Bazar or local businesses like Rajmandir in Indian metros and mini-metros’ are of high importance today. Garnering a higher shelf share in these means a larger market share overall; giving a sharp bump to their spread throughout the country.

“Rising to the challenge from Ecommerce, even the local Kirana shops and General Stores have added home-delivery and self-service to improve customer experience.”

Another channel which has gained significant importance for the FMCG brands are pharmacies, indigenously also called Chemist shops, acting as a channel to improve penetration in many cities. Most high-end personal products find good shelf space at these stores providing avenues for chains such as Wellness Forever and Noble Chemists, among many others, to grow as an alternative retail channel.

Then came the cold stores supporting demand for Ready-to-Cook and Ready-to-Eat products. Many of these products are distributed through a cold chain network, such as McCain fries or Sumeru seafood.

Other channels like HORECA, short for Hotel, Restaurant, or Café, also created a space for themselves in the last decade to make things interesting for the FMCG players. While an increasing number of channels can give anyone an impression of diminishing wholesale, the picture is quite the opposite. Wholesale distribution has only flourished for most big consumer goods players, continuing to be an effective way to enable sales without deploying additional sales teams.

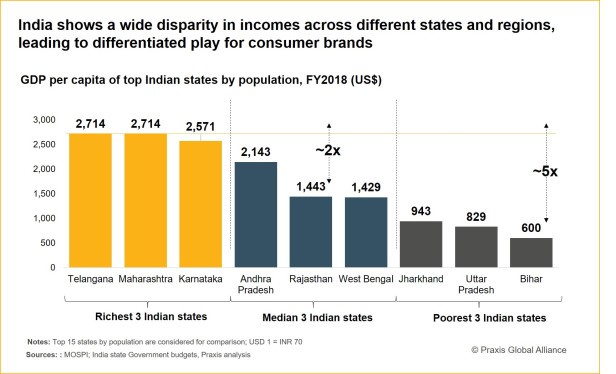

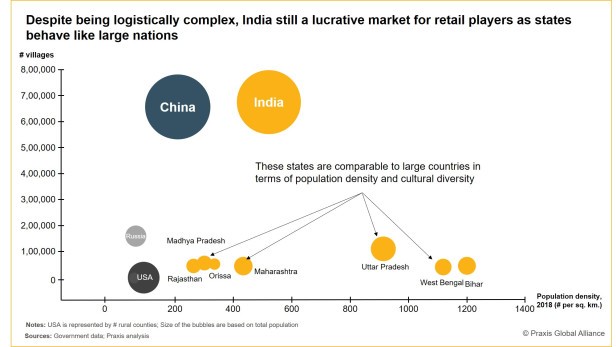

The great Indian powerplay: 1.3B people strong marketplace

While rural India was earlier considering an unattractive bet, things are now changing due to the immense opportunity present there. Taking advantage of the vast Indian demographic, most companies have forayed into rural distribution through the super distributor network. This helps companies reach micro interiors with efficient logistics and conserving working capital. Marico, GSK, and Dabur are some companies who have effectively used the super distributor model to reach small towns and villages.

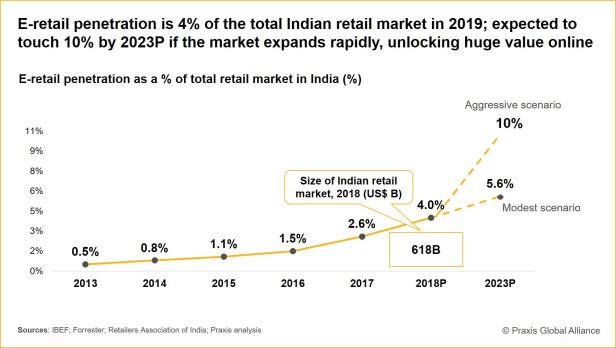

Today, while Ecommerce is making quick strides towards digital-led growth, all other channels of distribution have evolved for agility and experience too. As we move towards an omnichannel distribution strategy, there’ll be big changes in the delivery ecosystem to ensure delivery of anything, anytime and anywhere A recent Praxis Global Alliance study says, E-retail penetration in India is currently at 4% of the total Indian retail market and is expected to reach 10% by 2023P, which offers very high growth potential for FMCGs to capture the next wave of Ecommerce and digital customers.

Authored by

Madhur Singhal, Leader, Consumer and Retail Practice

Sandeep Zutshi, Leader, Consumer and Retail Practice